-

October is Fire Prevention Month: Your Local Fire Department Wants Everyone to be Safe

At Lindstrom Restoration, we work very closely with local fire departments. Over 20 local fire…

-

The Good, the Bad and Ugly of “Free Estimates”

At Lindstrom Restoration, we are sometimes asked to provide free estimates for projects. After all, isn’t…

-

Important Steps to Take with Water Damage

Lindstrom Restoration is here to provide prompt and efficient water restoration services, ensuring that your…

-

24/7 Professional Water Damage Restoration: Trust Experts to Dry & Restore Your Property

24/7 Professional Water Damage Restoration: Trust Experts to Dry & Restore Your Property At Lindstrom…

-

You’ve Had a House Fire. Now, What Happens?

You’ve suffered a house fire. Hopefully, no one was hurt. You wonder why this happened…

-

Why Choose an Insurance Agent Who Offers Value-Added Services

At Lindstrom Restoration, we often encounter clients who aren’t sure about their insurance details or…

-

Act Now: Have Your Roof Inspected for Hail Damage

Minnesota residents are quickly approaching a critical deadline to have their roofs inspected for hail…

-

Action You Can Take Now to Prevent Water in Your Basement and Check Available Insurance Coverage

Do you have water damage insurance coverage? The Problem: Excessive Rain Minnesota has recently shifted…

-

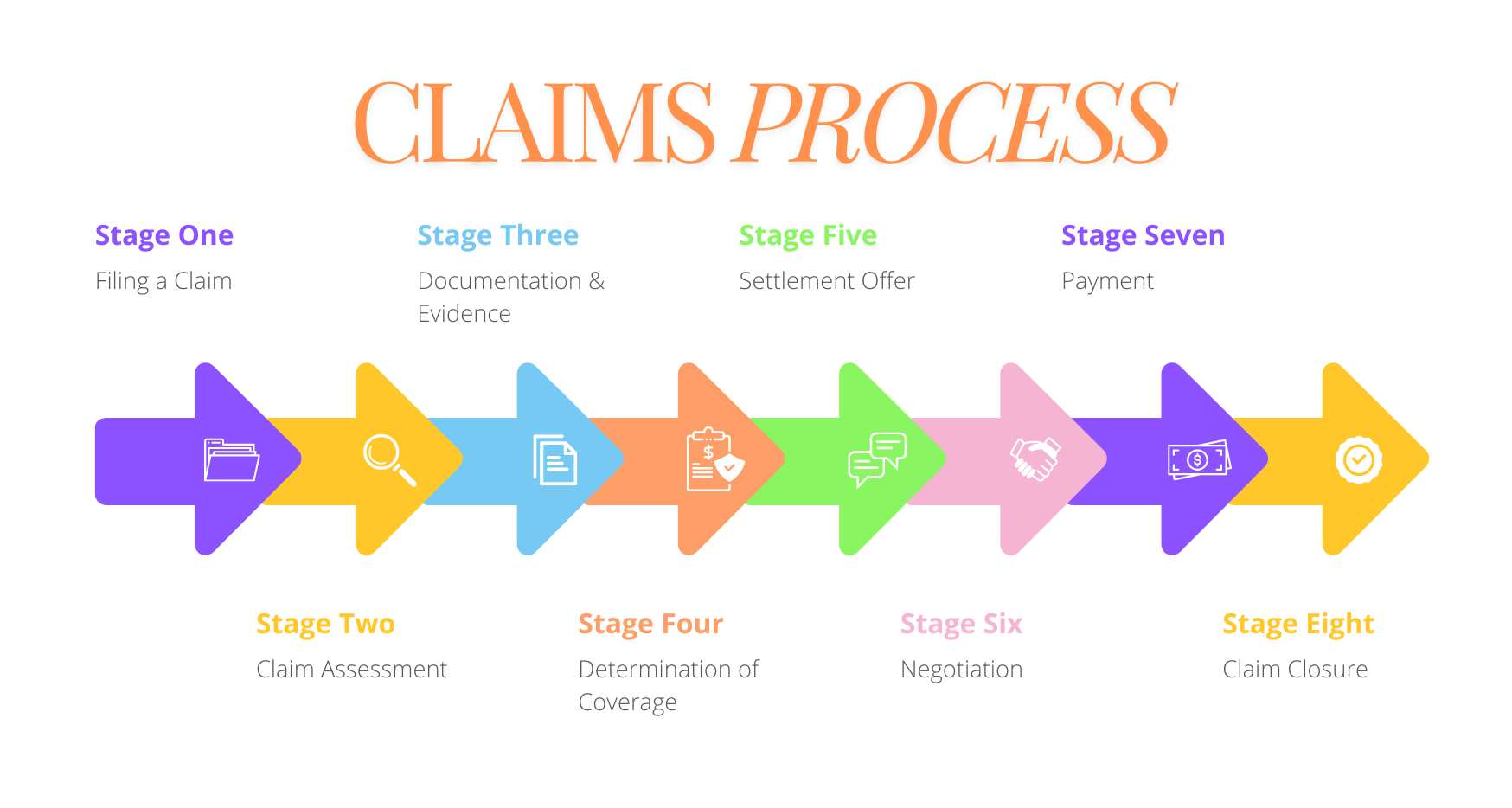

How Lindstrom Restoration Champions Customer Advocacy in Insurance Claims

In today’s increasingly contentious insurance claims environment, home and business owners need all the help…

-

Minnesota Insurance Rates

Insurance agencies across Minnesota echo a common concern: soaring rates. Whether speaking with a single-company…